Cement market special: Latin America

Cementos Argos

Cementos Argos

[1]

[1]

Photographer: Kaique Rocha

Photographer: Kaique Rocha

SC Corinthians

SC Corinthians

Dextra

Dextra

[2]

[2]

[2]

[2]

Loma Negra

Loma Negra

[2]

[2]

Votorantim

Votorantim

InterCement

InterCement

[2]

[2]

Cementos Argos

Cementos Argos

[2]

[2]

Cemex

Cemex

Holcim

Holcim

[2]

[2]

Cemento Pacasmayo

Cemento Pacasmayo

[2]

[2]

The cement industry in Latin America and other world regions is facing difficulties subsequent to the Corona crisis and due to inflation problems. Cement production has stagnated and for this year still no major improvements are projected. This article will look behind the scenes, present relevant up-to-date data and forecasts, as well as trends, and will profile the 5 major cement markets in the region.

1 Introduction

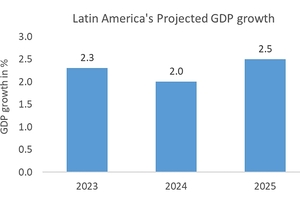

Latin America (incl. the Caribbean) had a population of 652 million in 2023. This is expected to grow by 10% to 715 million by mid-2035 and almost 15% to 750 million by mid-2050. In one of their recent economic reports [1], the IMF shows that the region has displayed remarkable resilience despite recent global challenges, rebounding from the pandemic more strongly than expected. Growth is moderating from 2.3% in 2023 to 2.0% in 2024 and 2.5% by 2025, as most economies are operating at potential (Figure 1). This year includes GDP growth projections of +2.2% for the LA7 countries, +2.2% for Brazil and Mexico, +1.9% for Chile, Colombia, Paraguay, Peru and Uruguay, +3.9% for the Caribbean and -1.9% for all other countries. Inflation in Latin America will continue on its downward trend from 16.6% in 2023 to 12.7% in 2024 and 6.5% by 2025. The IMF concludes that the risks to outlook have become more balanced [1].

However, according to the IMF and other sources, the region is currently experiencing the worst migration crisis in its long history. In addition to the traditional flows from Central America and Mexico to the United States, Cubans, Haitians, Nicaraguans and Venezuelans are also leaving their countries due to economic issues. For example, more than 7.5 million Venezuelans have already left their country since 2015. This situation is exacerbated by the increasingly devastating effects of climate change in Latin America, which have already caused deaths and significant economic losses due to hurricanes, floods and droughts. It is estimated that by 2025, 17 million people could be forced to flee their homes. Moreover, nearly 5.8 million people could fall into extreme poverty by 2030 due to the impact of climate change, especially because of a lack of potable water and increased exposure to excessive heat, droughts and flooding.

2 Latin America’s construction market

Urbanisation in Latin America continues, with 90% of Latin Americans expected to live in urban areas in 2050, up from 82% today (Figure 2), while the middle class has grown 50% in the last decade, now representing about 30% of the population. More than 23% of the population is below 15 years of age and only 9% is 65 and above. It is estimated that in Latin America the quantitative housing deficit affects more than 23 million people and the qualitative deficit, which includes deficiencies in materials, and the amount of basic services such as water, hygiene and transport facilities, affects more than 100 million people, together about 25% of the urban population. This has a tremendous impact on the housing sector, including affordable housing and infrastructure needs. Lots of studies have been made. Just for a country such as Colombia with 52.5 million inhabitants, about 400000 houses need to be built each year to satisfy demand.

Several projects are essential for the development of the region, improving the lives of its citizens, and driving economic growth. Infrastructure projects for example include Metro-Line 3 in São Paulo. This ambitious project, which shall be completed in 2025, has a budget of US$ 6.7 bn and will add 11.6 km of new metro line to Brazil’s Mega City and connect the Corinthians Arena (Figure 3). The Pacific Rim Highway in Peru is another mega project. This new highway, connecting Peru and Chile, will span 2700 km, to foster regional trade and integration. With an estimated cost of US$10 billion, the project is scheduled for completion by 2028. The Inga 3 Hydroelectric Dam in Ecuador shall generate clean and renewable energy for Ecuador, contributing to the country‘s energy security and sustainability goals. This 1400 MW hydroelectric dam has a budget of US$ 4.2 bn and shall be completed in 2025. Another highlight is the Bogotá Metro in Colombia. This 16 km metro line will link the city centre with the International Airport. The project shall cost US$5 bn and is expected to be completed already this year.

There are several more important infrastructure projects including roads, airports, harbours, energy, health and sanitation in the region. Examples are the 6.2 km Tnel de Ayacucho in Peru, the 500 km high-speed rail line Línea de Alta Velocidad Bogotá-Medellín in Colombia, the 100 km bus rapid transit system Transmetro de Santiago in Chile, the new International Airport of Mexico City (Figure 4), the Sofía City Project in Colombia, which is a 600-hectare mixed-use development to combine residential, commercial, and recreational spaces, the Atacama Solar Project in Chile, the 750 km Roraima Transmission Line in Brazil, the 1200 km water aqueduct Acueducto del Río Colorado in Mexico, the Hospital Geral de Brasília in Brazil, the Hospital del Niño in Peru and the Instituto Nacional de Cancerología in Colombia, dedicated to cancer treatment and research, to mention just a few of the many projects.

3 Market trends in Latin America

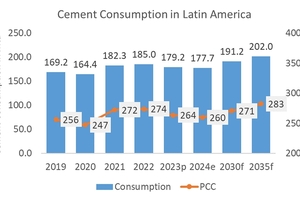

According to our projection, the cement market in Latin America and the Caribbean looks promising. Figure 5 shows the historical cement consumption from our latest report as well as an estimation for this year with forecast for 2030 and 2035 [2]. In 2023 the cement consumption contracted by -3.2% to 179.1 Mt/a, leading to a per capita cement consumption (PCC) of 264 kg/pcc. For 2024 we estimate a further decline in the consumption by -0.8%, which will result in 177.7 Mt/a and a decline of the PPC to 260 kg/pcc. For 2030 we see a moderate increase in cement consumption by an average CAGR of 1.2% to 191.2 Mt/a, while the PCC will slightly increase to 271 kg/pcc. Finally, for 2035 another increase in consumption by a CAGR of 1.1% to 202.0 Mt/a is projected. With an anticipated population increase to 715 million, the consumption figure will lead to a PCC of 283 kg/pcc.

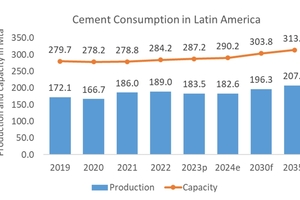

Looking at the cement production development in the region, this mainly depends on the future cement consumption as well on the net cement trade. In 2023 the net trade was 4.35 Mt/a, so more cement was exported than imported by the region. Figure 6 shows cement production and cement capacity development over the years with an outlook for 2035 [2]. In 2023 cement production was 183.5 Mt/a and cement capacity utilization was 63.9%. In 2024 both cement production and capacity utilization will decline. The outlook to 2035 forecasts an increase in cement production by 23.66 Mt/a, while cement capacity is projected to increase by 26.5 Mt/a. Interestingly, this leads to an increase in cement production utilization from 63.9% to 66.1%. However, this might also be influenced by other parameters, e.g. when cement plants have to be closed due to their CO2 emissions.

According to FICEM, the ‘Federación Interamericana del Cemento’, in the year 2020 about 128 Mt/a of CO2 were emitted by the cement producers in the region. Of these emissions, 116 are direct and 12 Mt/a are indirect ones [3]. According to FICEM, these emissions will grow to 218 Mt/a by 2050 if no further measures are taken to reduce CO2. In their projection FICEM indicates different methods to reduce CO2 emissions and achieve a net-zero cement & concrete production by 2050. These methods comprise what we know from the GCCA, and include higher efficiencies, co-processing of alternative fuels, lowering the clinker factor, using green cements, using green energy, re-carbonation, and last but not least, using CCS/CCUS technologies to capture CO2 for underground storage or for use in the production of fuels or other products. However, the region is far behind with CCS projects, as are many others in the world. Today, no full-scale CO2 projects are under design by the cement producers in the region [4].

4 Country highlights

4.1 Argentina

In Argentina, the four cement manufacturers Cementos Avellaneda, Holcim, Loma Negra and PCR operate 14 integrated cement plants and 3 grinding units with a combined cement capacity of 18.5 Mt/a. Loma Negra, which is majority owned by Intercement, is the largest cement producer in the country with 12.1 Mt/a capacity from 4 integrated plants and 3 grinding units, excluding the LomaSer blending and distribution facility. The cement plant L’Amali (Figure 7) in the Buenos Aires region, with its capacity of 6.0 Mt/a, is the largest in the country and one of the largest and most modern in Latin America. The new cement line at L‘Amalo Plant, inaugurated at the end of 2021, represents with US$ 350m and 2.7 Mt/a the largest investment in capacity in the last two decades. Last year, Loma Negra achieved their lowest GHG emissions with 503.5 kg/kg cement and a clinker factor of 69% in Argentina.

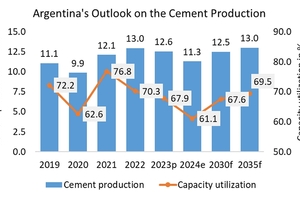

In 2023, Argentina produced 12.557 Mt/a of cement, which is a decline by -3.2%, when compared to 2022 (Figure 8). For this year, another decline by -10.0% to 11.3 Mt/a cement is projected. This will lead to a decline in the cement capacity utilization from 67.9% in 2023 to 61.1% this year. For the coming years, a slight increase in cement production to 12.5 Mt/a in 2030 and 13.0 Mt/a by 2035 is projected. This corresponds to a CACR of 1.7% by 2030 and 0.8% after 2030. We don’t see any major new capacity expansions in the next few years. Accordingly, with the larger cement production, cement capacity utilization will again increase to 67.6% in 2030 and 69.5% by 2035. The cement trade of Argentina is relatively small. The net trade was 0.059 Mt/a in 2023. This will not change much, and accordingly Argentina’s PCC will decline from 270 kg/pcc in 2023 to 242 kg/pcc in 2024. For 2030 and 2035 a PCC of around 260 kg/pcc is projected.

4.2 Brazil

Brazil’s cement industry is divided into 5 different regions, North, Northeast, Central-East, Southeast and South. Latest data show there were 72 integrated cement plants and 33 grinding units with a combined cement capacity of 94.0 Mt/a in 2023. The region Southeast with the States Minas Gerais, Rio de Janeiro, Sao Paulo and Espirito Santo is not only responsible for about 60% of Brazil’s GDP but also for about 46% of cement production in Brazil (2023). The cement market is fragmented, with 23 different groups and producers. The market leaders are Votorantim Cimentos, InterCement and CSN Cimentos, after the takeover of LafargeHolcim’s assets in 2021. Other larger producers are Grupo Joao Santos, Cimentos Mizu and Buzzi, which will have full control of Cimento National after taking over the 50% shares from Grupo Ricardo Brennand. CSN is in talks about taking over the shares of InterCement and thus becoming Brazil’s 2nd largest producer.

Votorantim operates a cement capacity of 34.4 Mt/a in Brazil, 10.7 Mt/a in the Southeast region, 9.5 Mt/a in the South, 7.3 Mt/a in Northeast and 6.9 Mt/a in the Central region (Figure 9). Votorantim has a global cement capacity of 57.3 Mt/a, another 1.6 Mt/a are in Latin America (Bolivia and Uruguay) while 8.2 Mt/a are in North America (USA and Canada). Cementis Artigas in Uruguay is a JV between Votorantim and Spanish-based Cimentos Molins. Brazil’s Companhia Siderrgica Nacional (CSN) has entered into an exclusive agreement to negotiate the acquisition of InterCement’s operations in Argentina and Brazil (Figure 10). The exclusive talks will run until July 12th, while CSN will conduct a due diligence process. Local sources indicate that CSN had offered around R$6 bn for the assets and would have to take on InterCement’s debts and carry out negotiations with the company’s creditors in the acquisition process.

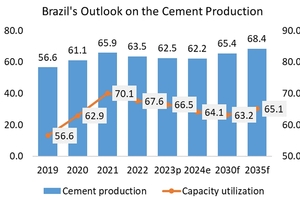

In 2023, Brazil produced 62.490 Mt/a of cement, which is a decline by -1.7%, when compared to 2022 (Figure 11). For this year another decline by -0.5% to 62.2 Mt/a of cement is projected. This will lead to a decline in cement capacity utilization from 66.5% in 2023 to 64.1% this year. For the coming years, a slight increase in cement production to 65.4 Mt/a in 2030 and 68.0 Mt/a by 2035 is projected. This corresponds to a CACR of 0.8% by 2030 and 0.9% after 2030. Capacity is projected to increase 11.0 Mt/a by 2035. Accordingly, cement capacity utilization will decline to 63.2% in 2030 and increase to 65.1% by 2035. The net cement trade of Brazil was 0.54 Mt/a in 2023. For the coming years, this will stagnate or decline slightly to 0.4 Mt/a. As a result, Brazil’s PCC will decline from 287 kg/pcc in 2023 to 285 kg/pcc in 2024. For 2030 and 2035, an increase in PCC to 292 and 299 kg/pcc is projected, respectively.

4.3 Colombia

PROCEMCO is the Colombian Chamber of Cement & Concrete. The organization represents Cementos Argos, Cemex, Holcim and a number of smaller producers in the concrete industry. There are 6 other smaller cement producers including Ultracem and Cemento Vallenato, who are operating cement grinding units. In total, in Colombia there are 20 integrated cement plants and 4 grinding units with a combined capacity of 19.0 Mt/a. The market leader is Cementos Argos with 26.2 Mt/a installed cement capacity from 12 cement plants,11 grinding units and 248 RMC plants in Colombia, the USA, Central America and the Caribbean (CAC). In Colombia the company operates 6 cement plants with a combined capacity of 8.5 Mt/a. The Cartagena plant (Figure 12) has become a flagship plant of the company. The strategic geographical location of the Cartagena port enables connectivity with the network of ports, terminals and grinding stations in other countries, which, together with its own fleet of vessels, represents an important competitive advantage.

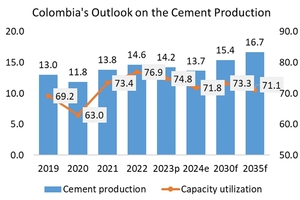

In 2023, Colombia produced 14.211 Mt/a of cement, which is a decline by -2.7%, when compared to 2022 (Figure 13). For this year another decline by -3.9% to 13.650 Mt/a cement is projected. This will lead to a decline in cement capacity utilization from 74.8% in 2023 to 71.8% this year. For the coming years, a moderate increase in cement production to 15.4 Mt/a in 2030 and 16.7 Mt/a by 2035 is projected, corresponding to a CACR of 2.0% by 2030 and 1.6% after 2030. For the next few years, capacity expansions by 4.5 Mt/a are projected. Accordingly, with cement production increases by 2.5 Mt/a, the cement capacity utilization will increase to 73.3% in 2030 and decrease to 71.5% by 2035. The net cement trade of Colombia was 1.318 Mt/a in 2023. This will not change much and accordingly Colombia’s PCC will decline from 247 kg/pcc in 2023 to 231 kg/pcc in 2024. For 2030 and 2035 a PCC of 262 and 273 kg/pcc is projected.

4.4 Mexico

Mexico has 6 cement producers, which operate 35 integrated grey cement plants and 1 grinding unit with a combined capacity of 61.8 Mt/a. Furthermore, there are 3 white cement production facilities with a capacity of about 1.0 Mt/a and 0.7 Mt/a production volume. The 6 cement producers are Cemex, Cemento Cruz Azul, Cementos Fortaleza, Cemento Moctezuma-Molins, Grupo Cementos de Chihuahua (GCC) and Holcim. The market leader in Mexico is Cemex. They operate 15 cement and grinding plants (Figure 14) in Mexico, 10 units in the USA market and 13 units in other Latin America and the Caribbean. Of Cemex’s total turnover of US$ 17.4 bn in 2023, US$ 5.1bn were generated in Mexico, US$ 5.3bn in the USA and 1.3 in other Latin American and Caribbean countries. The huge turnover in Mexico is also a result of 261 RMC plants and 13 aggregate quarries in the country. In 2023, despite larger production volumes, Cemex reduced scope1 CO2 emissions by 4%, due to record alternative fuel substitution rates.

Holcim Mexico is the second largest cement producer with 7 + 1 (white cement) plants and 13.3 Mt/a cement capacity. The company has a long history of operation in Mexico, having established Cemento Portland Apaxco in 1928, which was later changed to Cemento Apasco. Today, the Hermosillo plant (Figure 15) is a flagship of the company. Holcim is working on improving its carbon footprint. Together with co-operation partners, Holcim’s subsidiary Geocycle will install a 400 t/h plant to recycle construction and demolition waste (CDW). Cemento Cruz Azul operates the four integrated plants Hidalgo, Oaxaca, Puebla and Aguascalientes. With the inauguration of a 5th kiln line with 3700 t/d in the Oaxaca plant last year, Cruz Azul has been able to secure market shares against Cemex and its competitors in this growing country market.

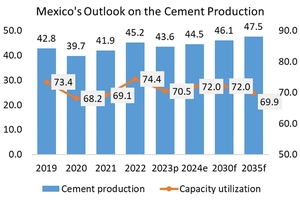

In 2023, Mexico produced 43.550 Mt/a of cement, which is a decline by -3.6% when compared to 2022 (Figure 16). For this year a moderate increase by +2.2% to 44.5 Mt/a cement is projected. This will lead to an increase in cement capacity utilization from 70.5% in 2023 to 72.0% this year. For the coming years, a slight increase in cement production to 46.1 Mt/a in 2030 and 47.5 Mt/a by 2035 is projected. This corresponds to a CACR of 0.6% by 2030 and after 2030. Capacity is projected to increase 6.2 Mt/a by 2035. Accordingly, cement capacity utilization will increase to 72.0% in 2030 before it declines to 69.9% by 2035. The net cement trade of Mexico was 2.1 Mt/a in 2023. For the coming years, this will be relatively constant or decline slightly to 2.0 Mt/a. As a result, Mexico’s PCC will increase from 317 kg/pcc in 2023 to 322 kg/pcc in 2024. For 2030 and 2035 an increase in PCC to 327 and 329 kg/pcc is projected, respectively.

4.5 Peru

Peru has five cement producers. These are Cementos Pacasmayo, Cemento Yura, UNACEM Peru and two smaller producers. These companies operate 9 cement plants with a combined cement production capacity of 18.5 Mt/a. The largest producer is Cementos Pacasmayo with a capacity of 4.9 Mt/a from the three plants Pacasmayo, Piura (Figure 17) and Rioja. Pacasmayo is the only producer in the North of Peru with the Pacasmayo plant as the flagship facility. In 2023, the company finished investing approximately US$ 83.5 million in a more efficient kiln for their Pacasmayo plant to increase its efficiency and reduce the carbon footprint. Yura, which is part of the Gloria Group, is the second largest cement producer with two plants in Arequipa and Cesur. The company was established in 1966. International expansion started in 2010 in Bolivia and now comprises 8 cement plants in 5 countries, also including Brazil, Chile and Ecuador.

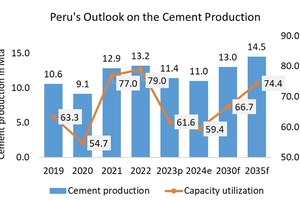

In 2023, Peru produced 11.404 Mt/a of cement, which is a decline by -13.6% when compared to 2022 (Figure 18). For this year, another decline by -3.7% to 10.980 Mt/a cement is projected. This will lead to a decline in cement capacity utilization from 61.6% in 2023 to 59.4% this year. For the coming years, a significant increase in cement production to 13.0 Mt/a in 2030 and 14.5 Mt/a by 2035 is projected, corresponding to a CACR of 2.9% by 2030 and 2.2% after 2030. For the next few years only a small capacity expansion by 1.0 Mt/a is projected. Accordingly, with cement production increases by 3.1 Mt/a, cement capacity utilization will increase to 67.7% in 2030 and to 74.4% by 2035. The net cement trade of Peru was still -0.13 Mt/a in 2023. These imports will further decline and accordingly, Peru’s PCC will first decline from 342 kg/pcc in 2023 to 324 kg/pcc in 2024. For 2030 and 2035 a PCC of 364 and 388 kg/pcc is projected.

5 Outlook

In 2024, cement production and consumption in most of the countries in Latin America are forecast to decline. In some countries such as Argentina, Colombia, Paraguay and Peru this can be a 2-digit or major decline. However, there are other markets in Bolivia, El Salvador, Mexico, Puerto Rico and probably Venezuela where there may be significant growth this year. In general, in the coming years cement market development looks more promising due to the growing housing and infrastructure needs. At the moment, the cement industry seems busy increasing alternative fuels rates and reducing the clinker factor as the most cost efficient measures to reduce the carbon footprint. There is a lack of CCS/CCUS projects. Some pilot stage projects have been started, but it looks like the first commercial scale project will not be installed before 2032-5.

onestone.consulting