Cement Market Special: India

UltraTech

UltraTech

IMF

IMF

OneStone Research

OneStone Research

Pexels

Pexels

National Portal of India

National Portal of India

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

OneStone Research

UltraTech

UltraTech

Ambuja

Ambuja

ACC

ACC

Nuvoko Vistas

Nuvoko Vistas

JK Cement

JK Cement

OneStone Research

OneStone Research

OneStone Research

OneStone Research

JSW Cement

JSW Cement

OneStone Research

OneStone Research

OneStone Research

OneStone Research

India aims to be the world’s third largest economy by 2030. Her cement industry is booming as never before. The main question is how long will this situation last. In the following market review a deep insight into India’s cement industry, the major producers and the challenges ahead are given. Investments, capacity expansions and decarbonisation efforts are described.

1 The economy

India has a population of 1.442 billion (mid 2024) and holds 5th place in the world’s GDP rankings for 2024 with US$ 3.94 trillion, corresponding to an annual GDP per capita of about US$ 2732. The International Monetary Fund (IMF) has upgraded India’s gross domestic product (GDP) in the current FY 2024-25 by 0.2% to 7.0%. However, the financial year by IMF is different to the fiscal year in India, FY 2024-25 = fiscal year FY’25 in India). While India’s economic growth slowed to a five-quarter low of 6.7% in the first quarter (1Q) of FY’25 from 7.8% in the preceding 4Q FY’24, development banks upheld their projection on India’s GDP growth for the current fiscal year FY’25 at 7.0% and for FY’26 at 6.6% (Figure 1). India’s growth projections by the IMF are 7.3% in 2024 and 6.5% in 2025, based on the calendar year. With this, India continues to maintain its position as the fastest-growing economy among emerging markets and developing economies.

While India’s aggregate economy remains promising, with the central government sticking to its fiscal consolidation roadmap, the fiscal policy in some of India’s states and union territories differs. In the recent Union budget, the central government projected it would bring down the fiscal deficit to 4.9% in FY’25 and 4.5% of GDP by FY’26. However, in recent months, many Indian states (which had elections last year or are due to have them this year) have promised an increase in welfare spending and stimulus, thus raising FY’25 fiscal deficit estimates significantly. Indian states together comprise more than 1/3 of the government’s revenue receipts, while they are responsible for 40% of capital expenditure and have a share of around 35% in public debt.

2 The cement and construction sector

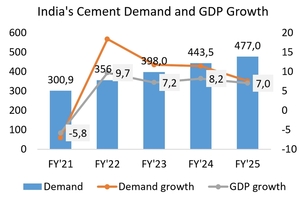

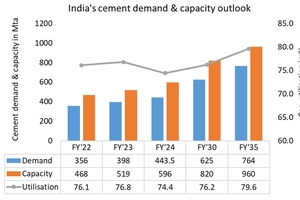

In India, the demand growth of the cement industry is considered as a multiple of the GDP growth, especially when the average 10-year cement growth vs. GDP growth is taken into account. While in the Capex cycle from FY’03 to FY’12 this average was 1.5x (1.5 x cement growth / GDP growth), the average declined to 0.6x from FY’13 to FY’24. However, the last period was significantly influenced by demonetisation in FY’17, credit tightness in FY’20 and the COVID-19 pandemic in FY’21. Figure 2 shows the cement demand vs. the GDP growth in the last few years with the preliminary data for FY’24 (current fiscal year is FY’25, starting April 2024) and the current year (FY’25). The projection for the last fiscal year is an 11.4% increase in cement demand to 443.5 Mta, which corresponds to 1.4x the projected increase of 8.2% for the GDP growth. However, the growth projections are quite vulnerable as the GDP growth of 6.7% in the 1Q FY’25 demonstrates.

An industry report came to the conclusion that India’s booming construction sector, which is driven by urban housing and the state spending on mega infrastructure projects (Figure 3) in new roads, rail, harbours and airports, could add up to 30 million new jobs by FY’30 on top of the current 70 million. Here are some data: It is anticipated that a construction of 20 million new rural homes is required by 2030. The rural home building subsidies have risen by 67% to US$ 2400 per home. The smart cities mission has been extended till FY’25. A pickup in private sector housing construction is expected with the investment of Rs.10 lakh crore (10 trillion) for the construction of 1 crore (10 million) houses in cities under the Pradhan Matri Awaas Yojana (PMAY) scheme. The allocation of the PMAY has increased by 18% from FY’24 to FY’25 to RS 26,170 crore. The share of India’s working age population in the total population will reach its highest level at 68.9% by 2030, leading to a higher homeownership.

India’s infrastructure sector is expected to become the largest driver for the country’s economic growth, with plans to invest RS 142 lacs crores on infrastructure between 2024 and 2030. For the budget FY’25 an outlay of Rs. 11.1 lakh crores for capital expenditure in infrastructure has been made, which represents 3.4% of the GDP. The national infrastructure plan has been expanded to 9735 projects. An ambitious target set has been drawn up for logistics and transport (Figure 4). The Indian Government’s Gati Shakti national master plan (NMP) for multi-modal connectivity shall improve India’s infrastructure. 48 Gati Shakti multi-cargo terminals were already installed by summer last year, while 35 multi-modal logistic parks are under development. Furthermore, 8300 km of high-speed rail lines are proposed for various routes. Phase IV of the Pradham Mantri Gram Sadak Yojana (PMGSY) project will be launched to provide all-weather connectivity to 25000 rural habitations.

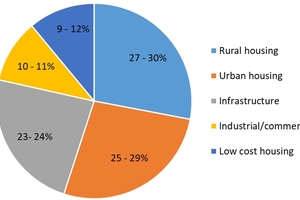

India’s cement demand mix has been relatively constant in the last few years (Figure 5). The largest share has been for rural housing and low-cost housing with 27 to 30% and 9 to 12%, respectively. Rural housing is followed by urban housing with 25 to 29%, depending on the year and quarter of the year. Infrastructure and industrial / commercial applications have been relatively small with 23 to 24% and 10 to 11% respectively. It can be expected that the infrastructure sector will emerge as the top sector in the coming years, with annual growth rates of 10-11% and a growth of at least 3 to 4% in the cement mix share, due to the Government’s commitment to boosting capital expenditure and encouraging private sector participation in infrastructure schemes. The Government has allocated another Rs. 2.5 lakh crores to railway system mega projects, continuing its focus on infrastructure.

3 The major cement producers

The Indian cement industry is highly fragmented with more than 30 producers, of which there are a few large players and several mid-size players. Large and mid-size players have used both organic and inorganic routes to grow, with significant consolidation trends in the past five years. The sector has seen a huge surge in mergers and acquisitions, resulting in the transfer of about 120 million t/a (Mta), of which almost 100 Mta have been acquired by large players. The region-wise installed cement capacity in India stood at 596 Mta at the beginning of FY’24. 111 Mta of this are in the North (Rajasthan, Punjab, Haryana), 130 Mta in the East (West Bengal, Chhattisgarh, Odisha, Jharkhand), 82 Mta in the West (Gujarat, Maharashtra), 190 Mta in the South (Tamil Nadu, Andhra Pradesh, Telangana Karnataka) and 83 Mta in the Central region (Uttar Pradesh, Madhya Pradesh). With a cement production of 444.7 Mta in FY’24, this corresponds to an average capacity utilisation rate of 74.6%.

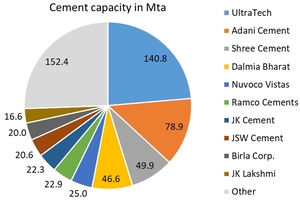

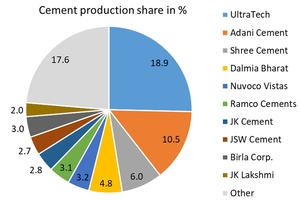

Figure 6 shows the cement capacity share of the TOP 10 cement producers in India for FY’24. The leading cement company is UltraTech, which is part of India’s Aditya Birla conglomerate, with 140.2 Mta cement capacity and 23.6% capacity share at the beginning of FY’24, followed by the Adani Group, which comprises Ambuja Cement, ACC and Sanghi Cement (excl. Dahej and Penna Cement, which were acquired later) with 78.9 Mta capacity and 13.2% market share. The next 2 places in the ranking are held by the large cement groups Shree Cement with 49.9 Mta (8.4%) and Dalmia Bharat with 46.6 Mta (7.8%), respectively. The next 6 places in the ranking are held by the mid-sized cement producers Nuvoko Vistas (4.2% market share), Ramco Cements (3.8%), JK Cement (3.7%), JSW Cement (3.5%), Birla Corporation (3.4%) and JK Lakshmi (2.8%). The TOP 10 producers comprised 74.4% of the capacity with growing market share, while all others comprised 25.6% market share.

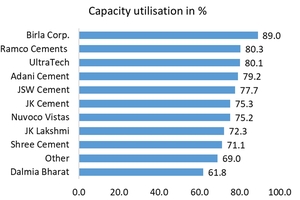

The production market share of the TOP 10 cement producers for FY’24 is presented in Figure 7, while the capacity utilisation rate of the producers is given in Figure 8. Highest utilisation rates have been achieved in FY’24 by Birla Corporation with 89% and a production share in India’s cement industry of 3.0%, followed by Ramco Cements with a capacity utilisation of 80.3% and a production share of 3.1% and UltraTech with a capacity utilisation of 80.1% and 18.9% production share. The lowest capacity utilisation rates were shown by Dalmia Bharat with 61.8% (4.8% production share), followed by the other producers with a capacity utilisation of 69% (17.6% share) and Shree Cement with a capacity utilisation of 71.1% (6.0% share). Anyhow, the average capacity utilisation is very dependent on the new cement capacity that has been made operational in the production year under review. Therefore, in many cases utilisation rates are more meaningful when regarded quarterly.

UltraTech increased its grey cement capacity to 140.8 Mta in March 2024. This capacity excludes the acquisition of Kesoram Cement with 10.75 Mta, awaiting regulatory approvals. In India the company operates 24 integrated plants (Figure 9), 33 separate grinding units, 1 clinkering plant, 1 white cement plant and 3 wall putty plants. The company also operates a 1.0 Mta cement plant in Bahrain, 4.4 Mta in the UAE and a 1.0 Mta cement terminal in Sri Lanka. Adani Cement comprised Ambuja Cement, ACC and Sanghi Cement with 78.9 Mta capacity and 88.9 Mta capacity if also Dahej and Penna Cement are included. The company operates 22 integrated plants (Figure 10) and 21 grinding units. The Adani Group has 24% of its capacity in the North region, 8% in Central, 25% in the West, 24% in the South and 19% in the East region. The highest utilisation rates are being achieved in the Central (108%) and East region (93%), while the lowest were in the South (65%) and West region (60%).

Shree Cement and Dalmia Bharat are the two cement producers which are also part of the large groups, with up to 50 Mta cement capacity. Shree Cement has a cement capacity of 49.9 Mta and a clinker capacity of 29.6 Mta from 4 integrated plants and 11 grinding plants. Beside the capacity in India, the company operates 4.0 Mta cement and 3.3 Mta clinker capacity in the UAE. The company is expanding its alternative fuel substitution rate from 3.5% in FY’22 to 15% in FY’24. It derives 51.1% of its power consumption from green power (211.5 MW WHR, 124 MW solar and 59 MW wind power). Dalmia Bharat, which is one of the market leaders in East India, has a cement capacity of 46.6 Mta and clinker capacity of 22.6 Mta from 15 production units (Figure 11). The company only had 5 plants in FY’14, with 11.8 Mta capacity. Alone 6.0 Mta of its new capacity was made operational in FY’24. The company had one of the lowest clinker rates in cement with 60.0% in 1Q of FY’25.

The mid-sized players with a cement capacity of up to 25 Mta, such as Nuvoko Vistas, Ramco Cement, JK Cement, JSW Cement, Birla Group and JK Lakshmi, have undergone healthy capacity growth, mainly led by organic expansion to new regions. The companies also focus on discipline in capital spending. Nuvoko Vistas rechristened from Lafarge India Limited and acquired NU Vista Limited (formerly Emami Cement Limited) and has 5 integrated units (Figure 12), 5 grinding units and 1 blending unit. JK Cement has a grey cement capacity of 22.34 Mta (Figure 13), as well as 3.05 white cement and wall putty capacity, and operates 77.5 MW coal-based captive power generation and 100.6 MW renewable power. JSW Cement, which also includes Shiva Cement, is part of the JSW Group, one of India’s largest conglomerates, and has the highest usage of GBFS from its blast furnace operations. The company is by far the largest user of GBFS in the cement sector in India.

4 Investments and capacity expansion

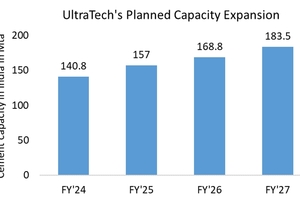

Indian cement producers are planning about US$ 14.3bn investments for capacity expansion over the next 4 years to FY’28. UltraTech plans to increase its grey cement capacity from 140.8 Mta in FY’24 to 157 Mta in this financial year, 168.8 Mta in FY’26 and 183.5 Mta by FY’27 (Figure 14), respectively, excluding 10.75 Mta Kesoram capacity. In this financial year, four more brownfield capacity expansions are included with the grinding units Arakkonam, Karur, Sonar Bangla and Durgapur, while in Maihar (Madhya Pradesh) a 4.5 Mta integrated plant will be commissioned and additionally two bulk terminals in Lucknow and Panval. For FY’26 the commis-sioning of five grinding units and one 1.2 Mta integrated plant in Nathware (Rajasthan) are foreseen. In FY’27, three grinding units shall be commissioned, of which two are greenfield units with 3.3 Mta each, while two 2.7 Mta integrated plants are planned in Andhra Pradesh as well as four new bulk terminals.

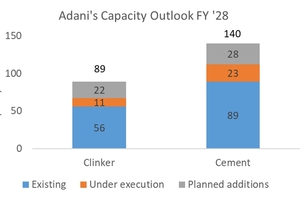

The Adani Group intends to increase its cement capacity from 88.9 Mta (including Penna Cement) in the 2Q quarter FY’24 to 112Mta by FY’26 and 140 Mta by FY’28. In this financial year the company will commission the Bhatapara 4.0 Mta clinkering unit and the three cement grinding units in Sankrail, Farakka and Sindri. In next FY’26 two clinkering units are planned, Maratha line 2 with 4.0 Mta and Jodhpur 3.0 Mta, as well as 10 grinding units in different states. The projects are under execution and the contracts for the major equipment have been awarded. In addition to this, 14 cement grinding units have been approved and are under progress (Figure 15).

Adani focusses on highly standardized plants. New standardized clinkering units shall have a size of 4.0 Mta (12000 t/d), while new standardized grinding units shall have a size of 2.4 Mta (7200 t/d on PPC basis). The company is expecting a high reduction of specific installation costs with this approach.

Nuvoko Vistas is one of the few larger cement companies which have not planned major capacity expansions. Instead, in this financial year only two railway sidings are nearing completion in Sonadith and Odisha. The Ramco Cements Limited (Ramco Cements) had earlier announced a capacity expansion plan to reach 26 Mta with a Capex of Rs 12.5 bn by FY’26. However, the company has upgraded the guidance to total installed capacity of 30 Mta by FY’26. JK Cement plans to increase its production capacity to 30 Mta by the end of FY’26. After setting up the Prayagraj grinding unit, the company ordered the main machinery for the 3.3 Mta clinker production and 1.0 Mta cement grinding unit in Panna as well as the additional cement grinding plants in Hamipur and Prayagraj with 1.0 Mta, each. Furthermore, the land needed for the 3.0 split grinding unit at Bihar has been acquired. The expansion is projected to cost approximately Rs 3000 crore, with Rs 700-800 crore already invested.

JSW Cement announced plans to set up an integrated steel plant, a power plant, a port facility and a cement plant at Jagatsinghpur in Odisha with an investment of Rs 65000 crore. While the steel capacity is projected to be 13.2 Mta, the cement grinding plant shall have a capacity of 10.0 Mta, mainly using GBFS (Figure 16). The company also filed for a Rs. 4000 crore IPO (Initial Public Offering) to set up a new integrated cement plant in Nagaur, Rajasthan and repay debts. The US$ 477 fresh equity will be mainly used for the financing of the 3.3 Mta integrated greenfield cement plant. The company has plans to hike the capacity of its cement business to 60 Mta over the next five years. Another mid-sized player, Birla Corporation, has managed to consolidate its operations and is ready to embark on the next phase of expansion (no targets have been published yet). JK Lakshmi Cement announced that their subsidiary Udaipur Cement Works Limited (UCWL) finished the commissioning of its 2nd clinkering unit, bringing their cement capacity to 4.7 Mta.

5 Decarbonisation

India’s cement industry is governed by guidelines ensuring quality, safety and environmental compliance. The Indian government has set a target to increase the share of alternative fuel use by the cement industry to 25% by 2030 as part of its commitment to reducing carbon emissions and promoting sustainable development. As of calendar year 2021, the share of alternative fuel in the domestic cement industry’s fuel mix was estimated at 5-6%, according to India’s Cement Manufacturers’ Association (CMA). Up to now, Ambuja (Adani Group) has achieved one of the highest thermal substitution rates of the Indian cement producers with 9.3%. The company has set a CO2 Net Zero commitment by 2050 with targets validated by SBTI (science-based Net-Zero Standard). Ambuja emitted 530 kg CO2/t cement in 1Q F’25, the 2030 target is 453, subsidiary ACC even came to 454 kg CO2/t CO2, having a target of 400 by 2030.

To achieve these ambitious targets, the leading cement producers in India follow three main routes: Substitution of fossil fuels with alternative fuels and increasing the thermal substitution rate, increase of green power through waste heat recovery (WHR) from the clinkering plant, as well as using solar and wind power, reduction of the clinker factor and finally introducing methods for carbon capture storage (CCS) and utilisation (CCUS). A report on CCUS in the Indian cement industry has been provided by the GCCA (Global Cement and Concrete Association) together with the Global CCS Institute and two other organisations [2]. However, in this report it is very difficult to find concrete projects by the Indian cement producers. The report highlights policy gaps and recommendations for India and provides benchmarks from the European and Canadian cement industry and states that in India there is a high potential for CCS projects.

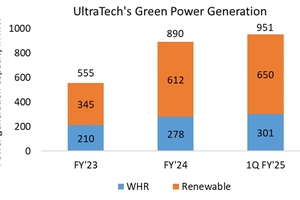

If we look closer at the Indian cement industry, we see huge developments in green power generation by the producers. Figure 17 shows the development of the green power mix by UltraTech. The target is to achieve 85% of green power for cement production in FY’30. The figure shows that WHR systems were increased from 210 MW in FY’23 to 301 MW in 1Q FY25, while the renewable energy (RE) from solar and wind power was increased from 345 MW to 650 MW. This means that in 1Q F’25 the green power mix of UltraTech Cement increased to 29.4%. Dalmia Bharat has one of the lowest net carbon footprints in the global cement industry with 467 kg CO₂ emission/t cement in Q1FY25, as well as one of the lowest clinker factors at 60% in 1Q FY’25. The company increased its solar and WHR power from 63 MW in FY’22 to 186 MW in 1Q FY’25. The company’s intention is to achieve net-zero CO2 emissions by 2040.

India is also the country with the lowest average clinker rate in cement. Some cement companies achieve blended cement ratios of about 85%, while Ordinary Portland Cement (OPC) has declined to around 15%. The average share of blended cements has been rising, with PPC (Portland Pozzolana Cement or fly ash cement) levelling at 62%, Portland Slag Cement (GBFS) levelling at about 10% and other Portland Composite Cements at 4%. The blending ratio has risen due to higher acceptance and applications of blended cement. Moreover, growth in the East region, and permission to use PPC from the State Public Works Department (PWD) were driving the increase in the blending ratio. The blast furnace slag production increased from 23.3 Mta to almost 31 Mta by 2024. More than 19 Mta of GBFS were used in the cement industry in 2023 [3]. While the availability of slag will be limited by production of steel through the blast furnace route, in India fly ash is still available in abundance.

6 Outlook

In 1Q FY’25 the cement demand remained muted in many regions of India, due to Union & State elections, extreme heatwaves, labour shortages, and early monsoon.

Accordingly, there are mainly different projections about the future cement demand in India and the corresponding capacity expansions. Optimistic projections see an annual average increase (CAGR) in the cement demand by more than 6% by 2030, while more pessimistic projections see a maximum annual average increase of +4.5%. In our projection (Figure 18), the cement demand will increase from 443.5 Mta by a CAGR of +5.9% to 625 Mta in FY’30 and a CAGR of +4.1% from FY’30 by FY’35 to 764 Mta. The cement capacity is projected to increase from 596 Mta in FY’24 to 960 Mta by FY’35. Accordingly, the cement capacity utilisation will increase from 74.6 Mta in FY’24 to 76.3% in FY’30 and even 79.7% in FY’35.