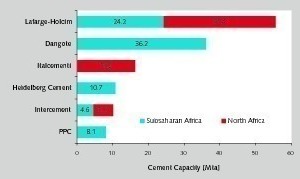

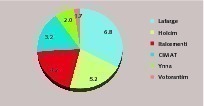

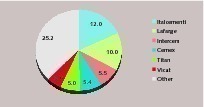

Lafarge-Holcim’s cement rivals in Africa

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

Lafarge

Lafarge

Dangote

Dangote

Dangote

Dangote

HeidelbergCement

HeidelbergCement

HeidelbergCement

HeidelbergCement

PPC

PPC

Vicat

Vicat

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

OneStone Consulting

Dangote

Dangote

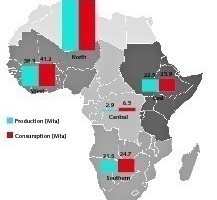

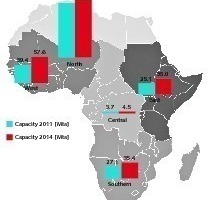

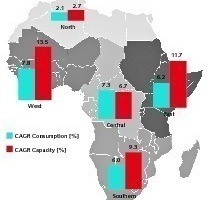

Once Lafarge-Holcim have merged they will be the leading cement producer in Africa with a capacity of about 53 million tons per year (Mta). However, there are a number of potential rivals, lead by the Dangote Group, which have massive capacity expansion plans in the pipeline. This market review outlines the latest cement industry trends in Africa, contains the latest 2014 market figures and looks at future plans of the major rivals.

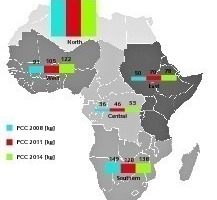

1 Introduction

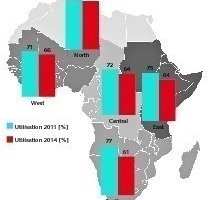

Africa has a population of 1.124 billion, 178 million (15.9 %) live in North Africa and 945 million (84.1 %) in Sub-Saharan Africa (Population Reference Bureau data mid 2014) but 50.6 % of all cement consumed in 2014 was in North Africa. As a result, the cement industry is characterized by a large variance in the per capita cement consumption (PCC) from north to south and also from east to west. While in 2014 the PCC in North Africa was 552 kg, in Sub-Saharan Africa it was just 102 kg. Highest PCC consumption in Sub-Saharan Africa was in Southern and West Africa with a PCC of 138...