Sustainable construction: green concrete alternatives

The construction industry is not short of ideas when it comes to sustainability. In fact, there is now an abundance of green and low-carbon concrete solutions available, many of which have been well documented and increasingly demonstrated at scale. From advanced supplementary cementitious materials (SCMs) to alternative binders and optimised mix-design strategies, innovation in this space is no longer the limiting factor.

The real question is no longer whether solutions exist, but whether the industry is prepared to adopt, industrialise, and normalise them.

If modern construction is serious about delivering on the commitments made during successive COP conferences, then the technical pathways are already visible. What remains is the collective will, across policy, standards, procurement, and risk culture to turn availability into impact [1].

1 From innovation to implementation

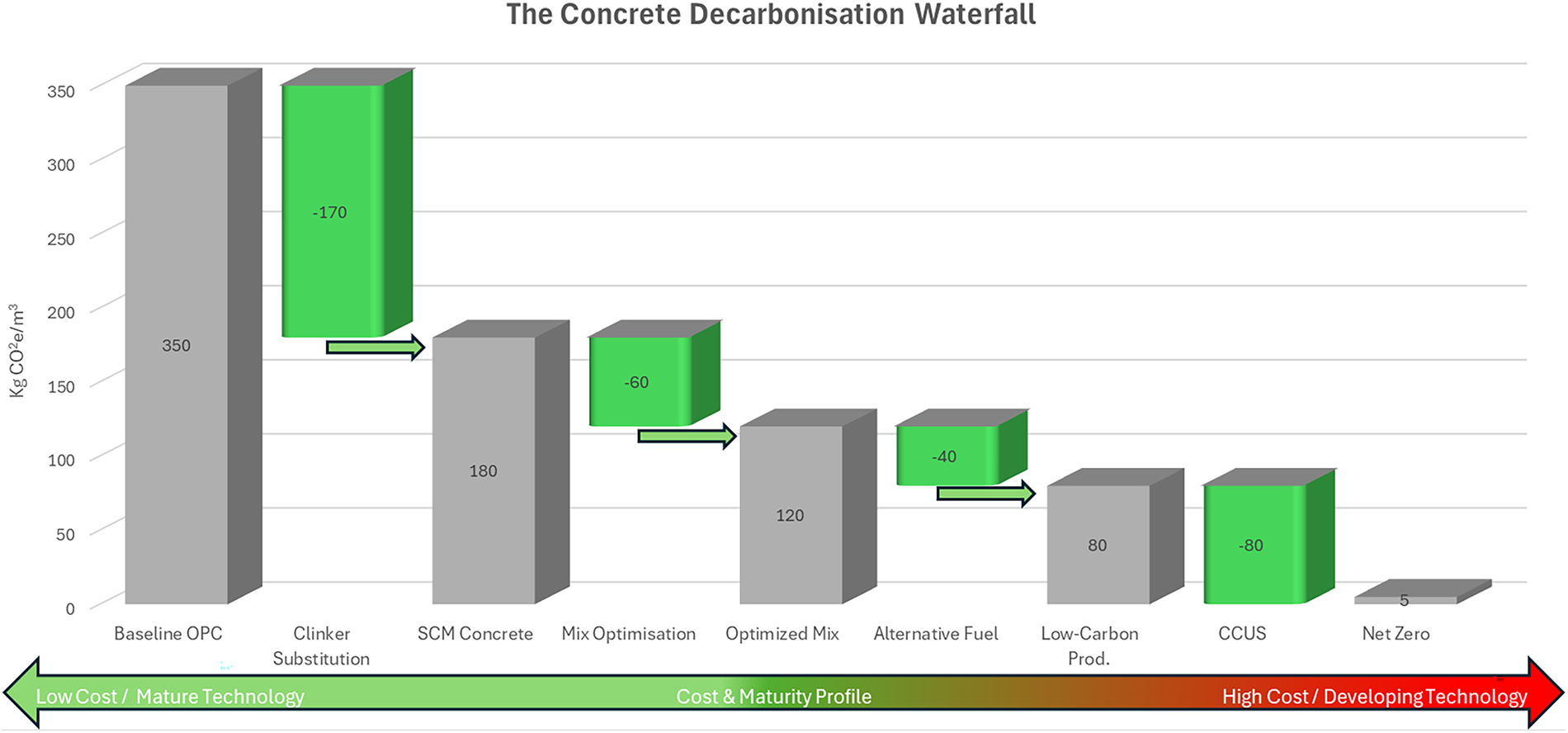

Over the past two decades, efforts to decarbonise concrete have focused on incremental improvements: energy efficiency, alternative fuels, and gradual clinker reduction. These measures have delivered meaningful progress and should not be understated. However, they are no longer sufficient on their own to meet the pace and scale of emissions reduction now required.

What has changed in recent years is the maturity of alternative solutions. Many green concrete technologies are no longer confined to laboratory environments or isolated pilot projects. They are being produced industrially, supplied commercially, and placed in real structures under demanding conditions.

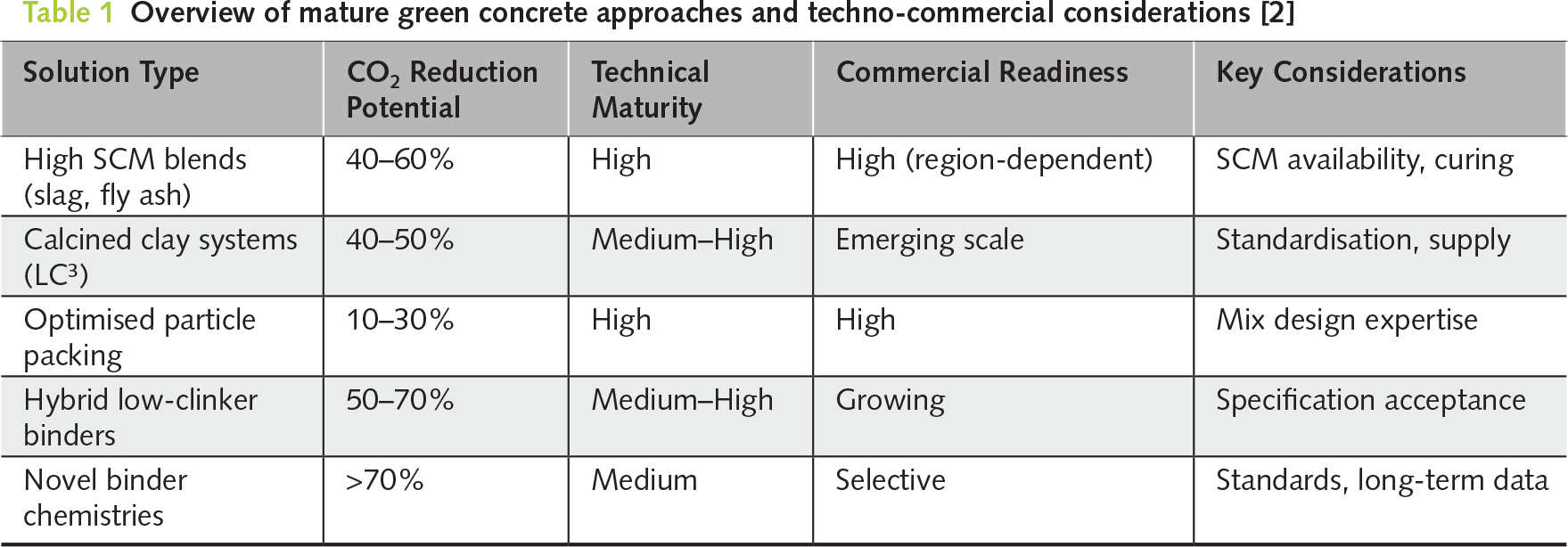

These include, but are not limited to:

• High-replacement SCM systems using slag, calcined clays, and emerging by-products.

• Optimised particle packing and activation strategies enabling lower cement contents.

• Hybrid binder systems combining multiple decarbonisation levers.

• Novel chemistries designed to significantly reduce clinker dependency

Across these methods, we are already delivering CO2 reductions of 40–70% in practical applications [2]. The challenge now lies not in proving feasibility, but in scaling adoption responsibly and economically.

Figure 1 Use of Low-Carbon concrete on extruded floor slabs

2 Acknowledging the friction: practical challenges and technical trade-offs

To view green concrete as a perfect “drop-in" replacement for Ordinary Portland Cement (OPC) is a mistake that overlooks genuine engineering hurdles. Low-carbon binders often present specific operational trade-offs:

• Strength Development: High-SCM mixes typically exhibit slower early-age strength gain, which can disrupt fast-track construction schedules and formwork striking times.

• Environmental Sensitivity: These materials are often more sensitive to ambient temperatures and curing conditions, requiring more rigorous on-site management.

• Operational Complexity: Most concrete plants are set up for a limited number of binders; introducing novel materials adds “silo pressure," increasing complexity and logistics costs.

3 The barriers to scale: inertia, logistics, and economics

The transition to low-carbon solutions is hindered by a deep-seated technological inertia, where specifications often remain anchored to 50-year-old “recipe based” codes. This “safety first” culture views any deviation from Ordinary Portland Cement as an uncompensated risk. This resistance is further compounded by a tightening supply chain: with coal plants closing, the geographic availability of traditional SCMs is becoming increasingly inconsistent [3]. Ultimately, without high carbon pricing or economies of scale enjoyed by the global OPC infrastructure, these alternatives continue to carry a “green premium” that makes them a difficult sell on raw material price alone.

4 Addressing the scepticism: durability, performance, cost

Predictably, scepticism persists. Questions around durability, long-term performance, constructability, and cost are frequently raised whenever low-carbon alternatives are discussed. These are valid concerns in an industry where structures are expected to perform reliably over decades.

However, it is increasingly clear that the technical questions are better understood than the commercial hesitation suggests. Many alternative solutions are now supported by:

• Long-term durability testing

• Field performance data under real exposure conditions

• Alignment with evolving standards and technical approvals

• Verified lifecycle and embodied carbon assessments.

The issue is not the absence of evidence, but the industry’s capacity to interpret and trust it at scale. Too often, unfamiliarity is treated as risk, while the embedded risks of conventional materials, including carbon exposure, are underappreciated. This imbalance slows adoption and keeps costs elevated by preventing scale, even as regulatory and market signals increasingly point toward change.

Figure 2 Use of low carbon concete on aggressive industrial environment

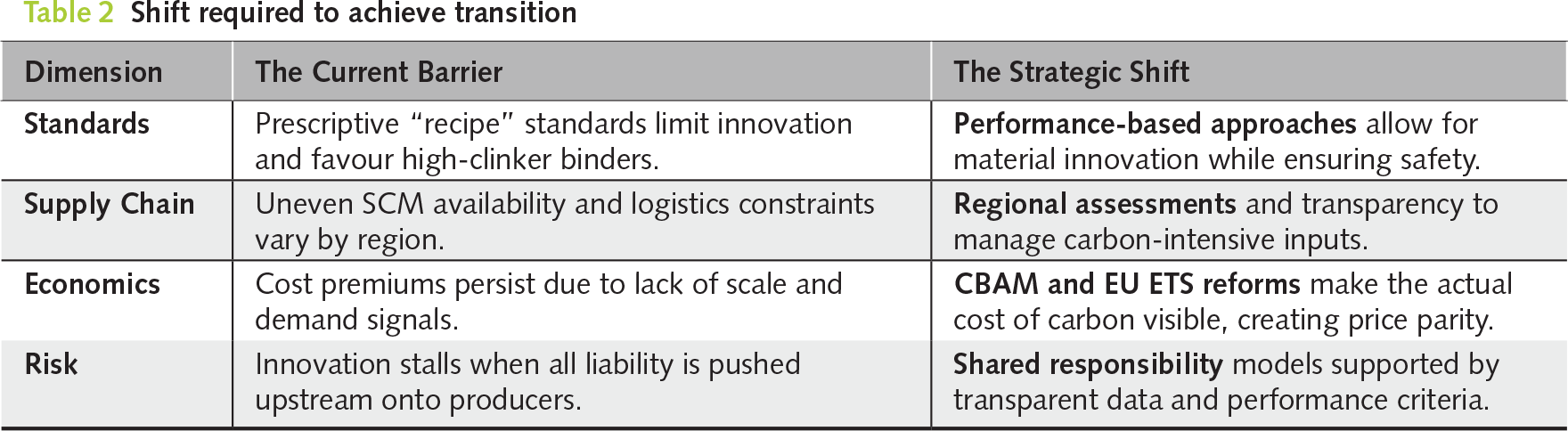

5 The techno-commercial reality

From a techno-commercial perspective, the success of green concrete alternatives depends on alignment across several interconnected dimensions. The following table summarizes the shift required to move these solutions from the margins to the mainstream.

6 The role of stakeholders and policy makers

While all actors in the value chain have a role to play, governments and public authorities hold a uniquely powerful lever. Through policy reform, procurement rules, and standards evolution, governments can:

• Signal long-term demand for low-carbon solutions.

• Reduce uncertainty for investors and producers.

• Encourage performance-based design approaches.

• Normalise innovation rather than treating it as an exception.

Public projects offer a controlled environment where novel solutions can be deployed with appropriate oversight, accelerating learning and confidence across the industry.

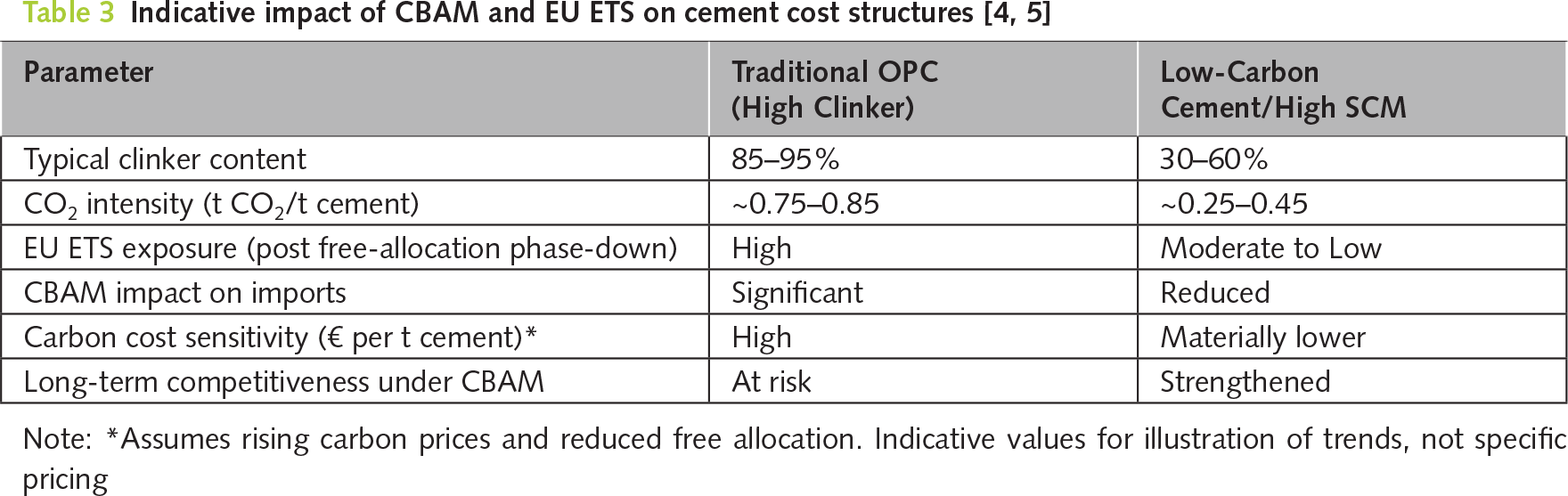

7 CBAM: from regulatory signal to market reality

An additional and increasingly decisive factor in this transition is the EU Carbon Border Adjustment Mechanism (CBAM).

In simple terms, CBAM ensures that imported carbon-intensive products entering the European Union face a carbon cost equivalent to that borne by EU producers under the Emissions Trading System [4]. Cement and clinker are among the first sectors covered. While the current phase focuses on reporting, the long-term implication is clear: carbon intensity will increasingly determine competitiveness, regardless of where a product is produced.

For the cement sector, this represents a structural shift. As free allocations under the EU ETS are progressively reduced and CBAM obligations take effect, the economic insulation historically afforded to clinker-intensive production diminishes [5].

In real terms:

• High-clinker products become more exposed to explicit carbon costs.

• Carbon credits evolve from a compliance buffer into a strategic liability.

• Low-carbon binders and high-SCM solutions gain a tangible commercial advantage.

CBAM does not mandate specific technologies, but it makes the cost of inaction increasingly transparent. In doing so, it reinforces the techno-commercial case for green concrete alternatives as both sustainability and risk-management tools.

8 Rethinking the role of ordinary portland cement

A complete replacement of Ordinary Portland Cement (OPC) may take many years and should not be the sole objective. OPC remains a reliable and well-understood material, supported by a global production infrastructure that cannot be transformed overnight.

However, CBAM and evolving carbon-credit dynamics fundamentally change how OPC should be viewed. The question is no longer whether OPC can perform, it can but whether continued reliance on high clinker content represents an acceptable long-term exposure to carbon cost and regulatory risk.

The more pragmatic path lies in maximising substitution, optimisation, and system-level efficiency, rather than pursuing binary replacement narratives [6]. Green concrete alternatives should therefore be seen as:

• Immediate enablers of emissions reduction

• Transitional solutions compatible with existing infrastructure

• Platforms for continuous improvement as standards and supply chains evolve.

Figure 3 Neto Zero Journey [1]

9 The importance of informed clients and specifiers

One of the most underestimated drivers of change is the role of the client [7]. In a healthy market, quality and performance expectations are ultimately defined by the client, not by the supplier.

An informed, demanding client, supported by competent designers and consultants, can accelerate innovation by:

• Challenging prescriptive specifications

• Accepting performance-based verification

• Valuing lifecycle performance over short-term cost minimisation

In a CBAM-influenced market, such clients also play a critical role in managing future carbon exposure at project level. Material choice increasingly becomes a strategic decision rather than a purely technical one.

The technologies exist. The data largely exists. The remaining challenge is alignment. Progress now depends on:

• Standards evolving in step with proven innovation.

• Procurement models rewarding outcomes rather than familiarity.

• Supply chains being developed with regional realities in mind.

• Carbon costs being transparently reflected in decision-making.

This is not only a technical challenge, but a leadership one. Organisations that can bridge materials science, commercial execution, and regulatory foresight will shape the next phase of sustainable construction.

If the construction industry is genuinely committed to sustainability with tangible results, now is the time to move beyond cautious observation and towards structured adoption.

Green concrete alternatives are no longer experimental curiosities. They are practical tools available today, capable of delivering meaningful emissions reduction while managing future carbon risk. What they require is attention, understanding, and opportunity.

The solutions are here. The regulatory and economic signals are clear. The responsibility to act is collective.