African cement & concrete decarbonization: challenges and opportunities for local innovation in the global setting

As a UNESCO Associated, CTCN Technical Assistance Provider, and independent scientific research trust, CSTI uses an EcoChemistry lens to identify solutions across multiple sectors. We identify large public-interest markets, such as low-carbon construction, pollution control, biodiversity restoration, and circular materials. We then develop evidence-based phasing frameworks combining science, standards, pilots, procurement pathways, and partnerships. Each stage reduces uncertainty and creates the right to scale into larger commercial, regulatory, or investment opportunities.

Based in Nairobi, we collaborate globally with those seeking to transform systems, not just materials, in ways that increase social and natural capital. Cement is characterized as the most environmentally damaging construction material because of its ubiquity and resource intensity. This also creates an unprecedented opportunity for systemic transformation. African cement markets are not yet highly integrated with locked-in supply chains or volumes. We view this as an opportunity to create a flexible, solution-focused cement and concrete manufacturing model that grows with versatility while deepening customized optimization.

Dr. Cecilia Wandiga, CSTI

2 Understanding African capacity

Africa’s cement decarbonization challenge is often presented as a technology gap. That framing is incomplete. The continent does not lack technical knowledge. African engineers, cement producers, contractors, materials scientists, quarry operators, masons, and informal construction specialists understand local sands, aggregates, pozzolans, clays, soils, curing conditions, and mix behavior with a depth that is often invisible to global climate finance. The real roadblock is not the absence of knowledge. It is the absence of funded systems that turn African knowledge into trusted, comparable, finance-grade data.

Instead of thinking of Africa as an ‘affordable market testbed,’ investors should view countries across the African continent as an opportunity to develop resource-optimized tropical admixtures, along with new production infrastructure models that deliver materials as a service instead of bulk. Africa’s vast and varied ecosystem landscapes are an opportunity to create low-impact, nature-sensitive admixtures.

3 Low impact chemical admixtures

An EcoChemistry pathway that could be common for African cement decarbonization is the pozzolanic reaction, where reactive silica and alumina from volcanic ash, calcined clays, rice husk ash, or other locally characterized materials react with calcium hydroxide from cement hydration to form additional C-S-H and C-A-S-H binding gels. This reduces emissions by lowering clinker demand, while optimized particle size distribution and compatible water-reducing admixtures can reduce the water needed to achieve workable concrete. The opportunity is not simply to add “local materials,” but to chemically fingerprint African pozzolans so their mineralogy, surface charge, particle size, contaminants, and water demand can be engineered into reliable low-carbon concrete systems.

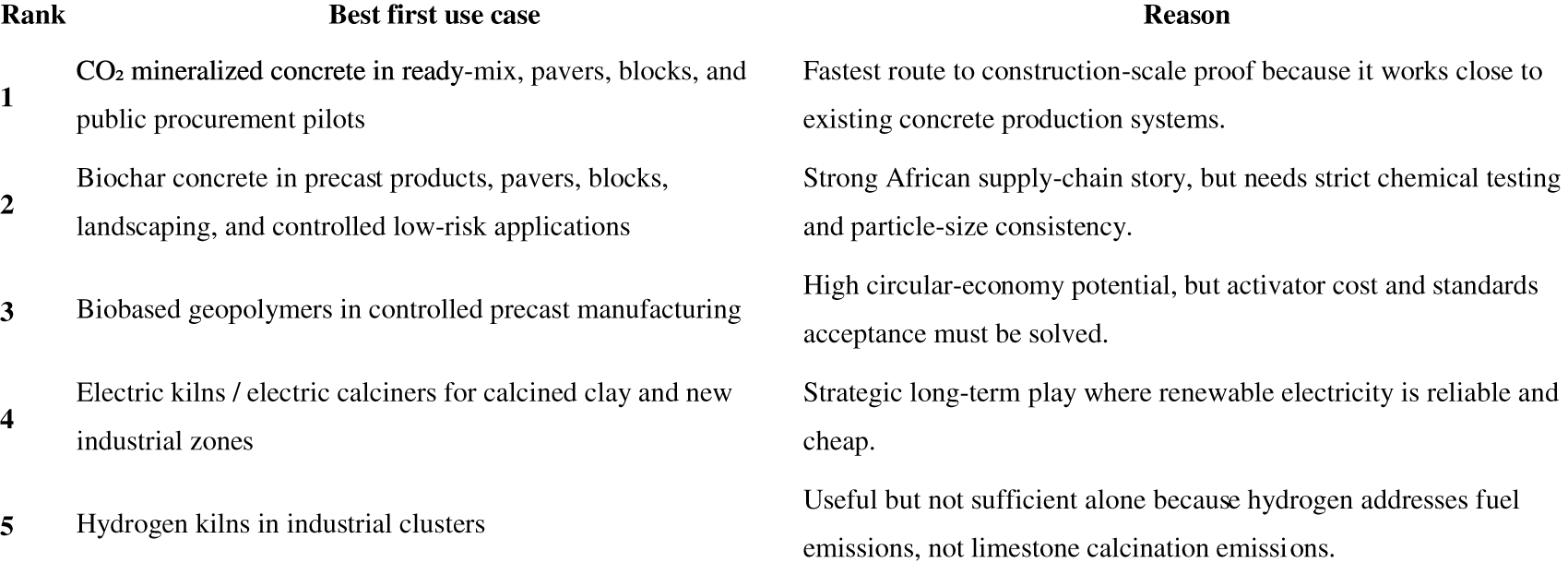

3.1 CSTI’s African priority ranking for decarbonization

New product development is the most expensive part phase of the NetZero journey [1]. Before changing kiln technology [2], cement manufacturers can test the downstream market by partnering with innovation companies focused on low carbon concrete admixtures that are optimized for their brand specific cement classes. The resulting market feedback reduces the risk of overestimating the ‘green premium’ [3] by providing data on when demand for low carbon materials is enough to justify kiln, fuel, and cement admixture alterations.

Image credit: octavia carbon

4 Natural resources and waste residues

Africa’s geology and biomass systems create a second layer of opportunity beyond pozzolanic substitution. Volcanic rockbeds and basaltic formations can support direct air capture and storage and CO2 mineralization pathways [4], creating room for partnerships such as Octavia Carbon and Cella working with Zen Carbon to develop captured CO2 cement mineral storage and low-carbon concrete production.

At the same time, rising demand for indigenous acacia species agroforestry, such as Seedalls Kenya biochar, invasive species removal, and credible carbon dioxide removal markets can create a controlled feedstock base for waste-residue biochar concrete [5], as emerging examples like Pyrogen suggest. Africa’s cement production infrastructure also has a strategic timing advantage: in many markets, outdated kilns and underscaled capacity mean there is less locked-in legacy equipment to defend, making it possible to design new production models around electric kilns, electric calciners, or other low-carbon heat systems.

As green hydrogen capacity in cement kilns develops [6], it may also become a targeted substitute for coal, diesel, and petroleum-based fuels in industrial clusters, especially where renewable power, water governance, and gas-handling infrastructure can support safe and cost-effective deployment.

Image credit: octavia carbon

Image credit: zen carbon

5 Global alignment through data

The alignment problem in Africa is that most current pilots are plant-scale, not construction-scale. A plant-scale pilot asks: can the producer manufacture this material? A construction-scale pilot asks a more difficult question: can the whole value chain trust it? That includes the cement producer, ready-mix supplier, contractor, structural engineer, architect, quantity surveyor, developer, regulator, insurer, bank, carbon buyer, and public procurement authority. Each stakeholder needs a different layer of evidence.

Image credit: zen carbon

The result is fragmentation. One company tests calcined clay. Another tests biochar. Another tests CO2 mineralization. Another tests alternative fuels. Another optimizes the mix design. Yet the evidence does not accumulate into a national or regional confidence system. Investors then hear many promising claims but see limited comparable proof. Engineers remain cautious. Regulators hesitate. Public procurement defaults to familiar materials. Banks price the risk too high. The green premium survives because the learning curve is not being converted into market trust.

China’s cement emissions database model is instructive. Databases such as the China Cement Emission Database (CCED) and the GID-Cement Emission Database (GCED) point toward a more strategic approach: emissions reduction is not credible unless it is mapped, measured, and comparable across facilities, technologies, regions, and time.

The CCED provides intensive unit-based information on activity rates, production capacity, operation status, PM, and NOx control technologies for over 3100 clinker production lines and over 4500 cement grinding stations. The GCED provides up-to-date elementary information and high-resolution emissions from global cement plants, which includes plant-level, national, and regional capacity and age information, as well as anthropogenic emissions of CO2 and various air pollutants (SO2, NOx, primary PM, VOCs, CO, black carbon, and organic carbon).

Africa needs its own cement and concrete emissions evidence base, built around African materials, African construction conditions, and African infrastructure priorities.

Africa’s opportunity is to create a cement decarbonization data platform that links five layers.

First, material characterization. This should include chemical composition, mineralogy, particle size distribution, heavy metals, organic contaminants where relevant, moisture, loss on ignition, reactivity, and variability across local sources.

Second, performance testing. Low-carbon materials must be evaluated against real construction requirements, not only laboratory curiosity. Strength, setting time, workability, durability, curing sensitivity, water demand, admixture compatibility, and field performance should be captured in a structured format.

Third, emissions accounting. African databases must include clinker content, fuel emissions, electricity emissions, transport emissions, SCM substitution, carbonation, CO2 mineralization, and end-of-life assumptions where relevant.

This is the missing bridge. Each pilot should be linked to a real project application: pavers, blocks, slabs, roads, drainage works, housing, industrial floors, foundations, or public buildings.

Fifth, procurement and finance translation. Data must be converted into decision tools: performance-based specifications, model tender language, risk allocation frameworks, insurance guidance, lender due diligence templates, and carbon-benefit reporting.

The biggest opportunity for Africa is that its cement demand is still growing. Unlike mature markets, where decarbonization often means retrofitting locked-in infrastructure systems, African markets can build better evidence systems early. Urbanization, housing demand, transport infrastructure, climate adaptation, and industrialization all require cement and concrete. If Africa builds the right data infrastructure now, it can avoid copying high-carbon construction pathways and instead create regional low-carbon material economies.

The investable African opportunity is not “green cement” as a generic product. It is a verified low-carbon construction materials platform: local materials testing, construction-scale pilots, embodied-carbon databases, performance-based specifications, and procurement-ready MRV. Previous ZKG articles support this framing: solutions fail when they do not integrate, scale, or overcome the green premium; and green concrete adoption depends on standards, supply chains, economics, and risk-sharing rather than technical invention alone.